Table of Content

VA Loan FAQsAre you considering taking advantage of your VA loan benefit? You had a foreclosure on a previous VA loan and did not repay the VA in full. You had a compromise claim or short sale on a previous VA loan and didn't repay the VA in full. You have used your home loan benefit, but had a foreclosure or compromised claim (i.e. short sale) and repaid the VA in full. Review any closing documents in advance so that you are ready to sign them when the time comes.

You've estimated your affordability, now get pre-qualified by a lender to find out just how much you can borrow. As of January 1, 2020, VA-eligible borrowers can get any size loan with no down payment. Whether you’re considering a VA loan, conventional mortgage, USDA loan or an FHA loan, getting preapproved is a big milestone in your homebuying journey. Talking to a VA lender about your home loan affordability is always a smart first step during the homebuying process. However, powerful tools exist that eliminate the fear of purchasing a home you can’t afford, and doing so will give you a realistic idea of how much VA home loan you can afford.

Explore personal banking

According to recent Census Bureau data, Arlington’s median home value is $669,400 and its neighbor Alexandria, is at $557,000. The $274,300 median home value in Virginia Beach seems relatively affordable compared to its neighbors in the north. And if you’re looking for more savings, Richmond comes in at $220,700 - not bad for the state capital. Virginia is the 12th-most populous state in the U.S. with an estimated 8.6 million residents, according to the U.S. The state takes up about 42,800 square miles, and is close in size to Tennessee. The northern and eastern edges of the state hold most of the population.

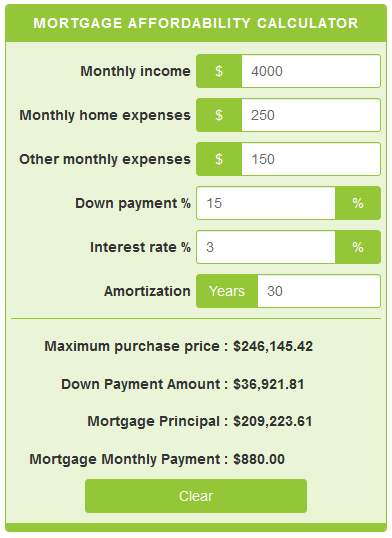

Several determinants could affect your interest rate, including credit score, current mortgage rates, downpayment, credit history, and loan term. A VA loan mortgage calculator is a tool for estimating your monthly payments. One of the first steps in the homebuying process is determining your price range. Our VA loan affordability calculator gives you an estimate of how much you could afford using a VA home loan based on your financial situation. Ideally, you’ll want to leave a buffer for savings and unforeseen expenses.

Other Homeownership Expenses

You had a deed in lieu of foreclosure on a previous VA loan and transferred the home's title to the bank that holds your mortgage to avoid foreclosure. You have paid a previous VA loan in full and sold the property . Refinance calculatorInterested in refinancing your existing mortgage? Use our refinance calculator to see if refinancing makes sense for you. Find a lender on Zillow and discuss your VA loan eligibility with a lender who understands the VA loan process.

Here is a mortgage rate table listing current VA loan rates available in the city of Los Angeles and around the local area. But, as discussed, the VA sets some home loan requirements, but it doesn’t actually lend money. In other words, just because you meet VA DTI criteria to borrow $380,000 doesn’t mean your lender will actually approve a loan of that size.

Down Payment

It was signed into law by President Franklin D. Roosevelt as an alternative to bonus checks to improve the economic standing of military members and veterans. Money that you can spend on the down payment and closing costs. Use our VA home loan calculator to estimate how expensive of a house you can afford. The principal is what you’ll pay every month towards the loan balance, while the interest is the amount you pay your lender for lending you the money. The number of years you have to pay off the loan (assuming you haven’t made additional principal payments). The VA requires no down payment, unlike other loan types, which generally require at least 3 to 10 percent.

Borrowers with an existing VA mortgage can apply for VA interest rate reduction refinance loans . This special type of refinancing allows borrowers to reduce their current mortgage payments. Because it refinances your loan, you have the option to change your rate and loan term. Take a conventional loan if you have enough funds and a good credit score. This is beneficial especially if you can score a low rate while avoiding monthly PMI payments.

Get the Military Insider Newsletter

If you hire an attorney to review the contract, you’ll owe him or her a piece of the pie. Title insurance covers problems or hidden risks that affect your ownership rights. Most lenders require buyers to buy a policy to insure the mortgage loan. Buyers have the option to add an additional policy to cover the difference between the loan and the home value.

SmartAsset’s Closing Costs Study assumed a 30-year fixed-rate mortgage with a 20% down payment on each county’s median home value. We considered all applicable closing costs, including the mortgage tax, transfer tax and both fixed and variable fees. Once we calculated the typical closing costs in each county we divided that figure by the county’s median home value to find the closing costs as a percentage of home value figure.

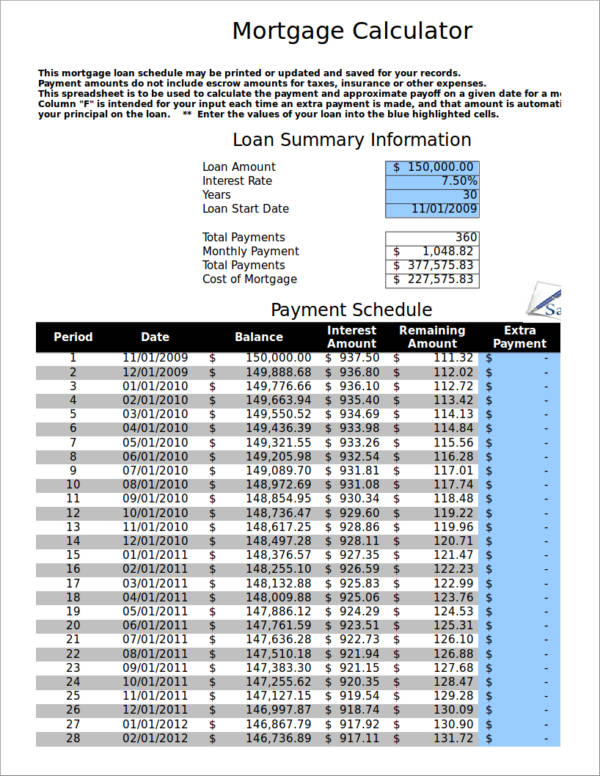

Below is a summary of the inputs and calculations used to calculate estimated payments and closing costs. After you calculate the mortgage payment and the loan amount you believe you can afford, give us a call and let us get right to work for you. We’re available 7 days a week to help pre-qualify you for the perfect loan, working on your schedule, not ours.

You must get your COE, satisfy the lender’s requirements, and meet all the MPRs. Veterans are in the clear, but if you are an active military member, you might get a PCS. Here are the steps to using a basic VA mortgage loan calculator.

By using, you will be matched with participating members of the ICB Solutions network who may contact you with information related to home buying and financing. These members typically have paid to be included but are not endorsed by ICB Solutions, LLC or this site. The interest rate is a percentage of the amount borrowed charged to the borrower. Your ultimate interest rate may differ; rates in the calculator are for informational purposes only. Any borrower with a DTI above 41 percent can still get one, but the process may require more investigation into your finances.

No comments:

Post a Comment